5 Steps to Handling High Inflation

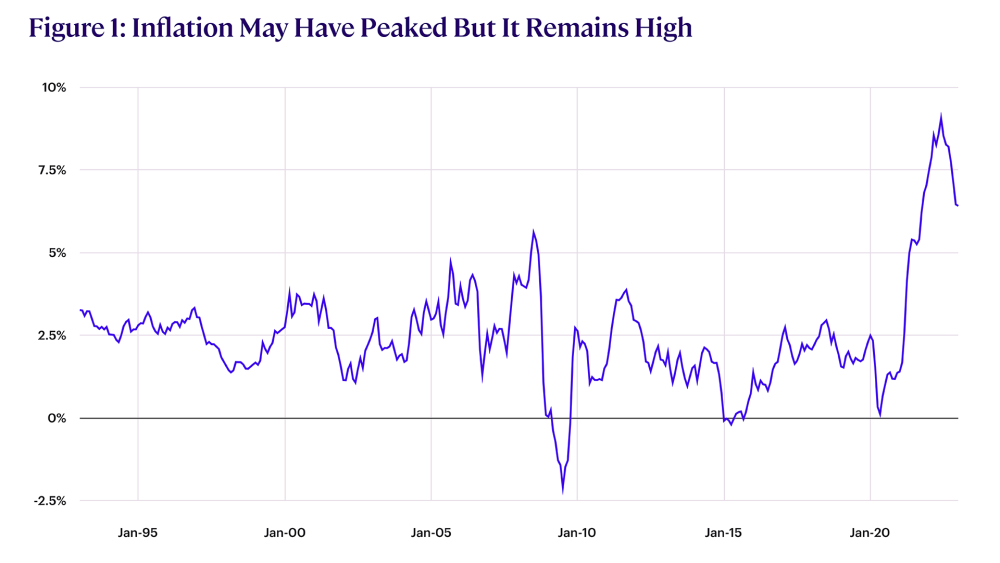

While the pace of inflation has slowed, it remains uncomfortably high (see Figure 1). Consumer prices continue to rise, and persistent inflation is eroding the value of savings and – combined with rising interest rates and struggling markets – hurting investors.

The good news is that there are practical steps you can take to reduce the impact of inflation on your family, budget, and portfolio.

Step 1: Do Not Panic

While inflation can be a source of stress, it is important to maintain perspective. Although prices are high and still rising, most households have a surprisingly robust capacity to adjust to high inflation and there are many things you can do to protect yourselves and your family.

So, do not allow yourself to become overly stressed – instead, focus on what you can do to thrive despite high inflation.

Step 2: Review Your Income

If you are currently employed, consider the impact inflation has had on your income. Has your salary kept pace, or have you accepted a stealth pay cut as inflation eats away at the value of your paycheck?

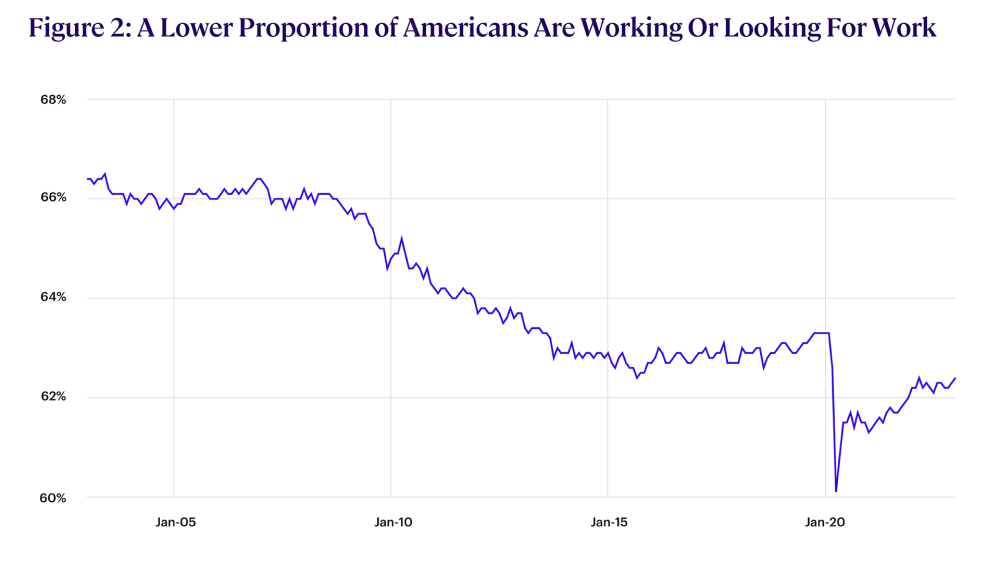

Remember, despite some easing, labor markets remain tight, with the labor force participation rate – which measures the proportion of Americans that are either employed or seeking employment – still well below pre-pandemic levels (see Figure 2). If your income has not kept up with inflation, it may be time to consider a new job.

For those in retirement who are worried about their income, there was some good news on the Social Security front – Social Security checks were increased by 8.7% for 2023 to account for higher inflation.

However, if you are drawing an income from your retirement savings, talk to your financial advisor. You may need to increase your drawdown rates to cover today’s higher cost of living but this may pose a risk to your long-term plans. Your advisor can help you balance your need for higher income against the need for capital preservation.

Step 3: Review Your Expenses

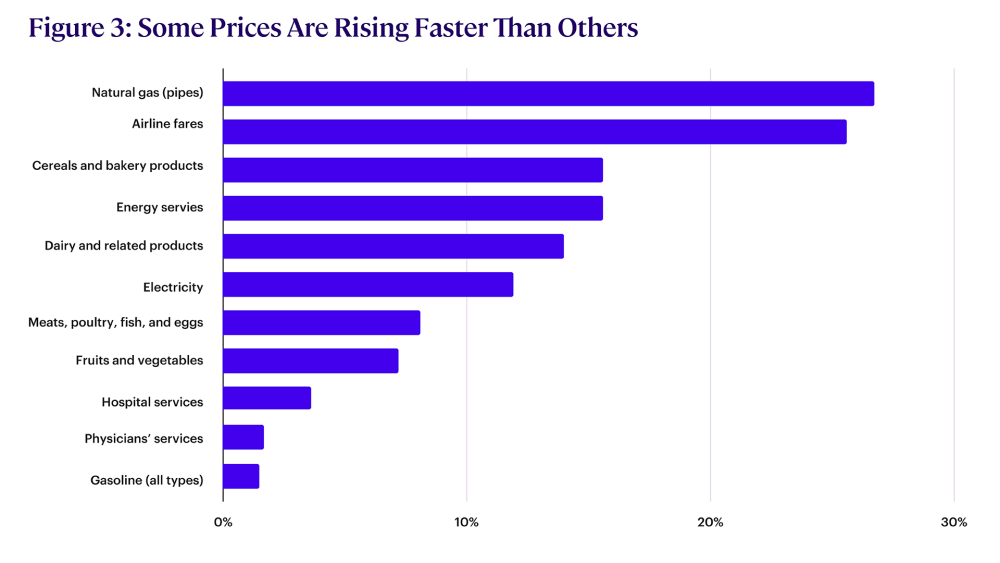

As prices rise, it makes sense to review your spending and budget. Some products and services have seen more significant price spikes than others, so adjusting your activities to reduce your exposure to especially expensive items can improve your personal inflation rate (see Figure 3).

For example, you could plan a vacation within driving distance to avoid high airfares or use an air fryer rather than a gas stove to prepare your meals.

Step 4: Review Your Debt

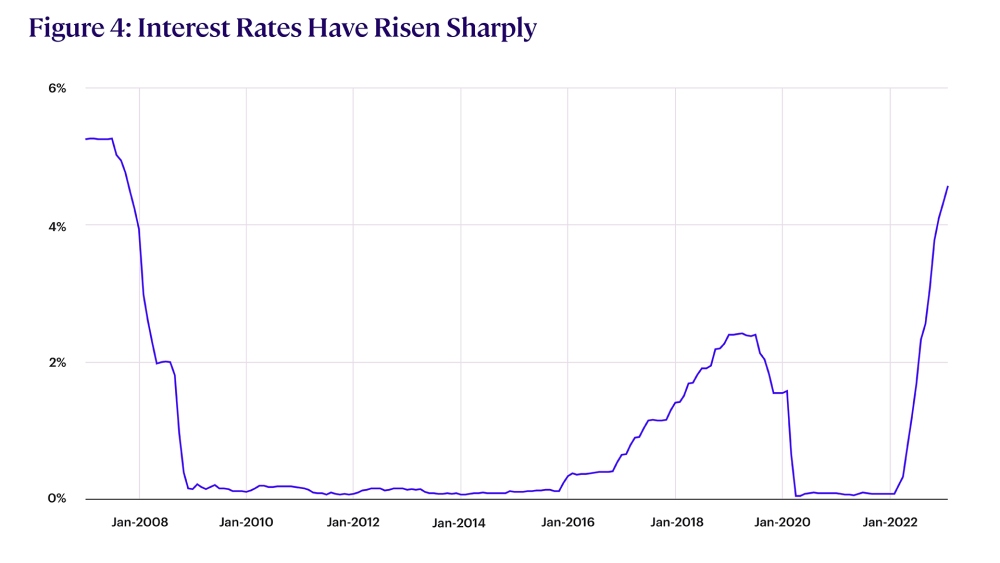

To fight inflation, the US Federal Reserve has been steadily raising interest rates, which are now at their highest level since 2007 (see Figure 4).

As rates rise, payments on variable-rate debt rise, and this could be putting a squeeze on your budget. If possible, therefore, it makes sense to pay down variable-rate debt or to consolidate it into a low-rate or fixed-rate pool.

Step 5: Check Your Portfolio

The key to financial well-being is generating inflation-beating returns. But after the painful contraction in asset prices over the last two years, you may feel that this goal is unachievable.

However, by making sure you have a balanced and diversified portfolio, you can set yourself up for long-term success. Review your portfolio and make sure you include allocations to assets that have traditionally served as a hedge against inflation, such as real estate, Treasury Inflation-Protected Securities (TIPS), or gold. This, combined with risk-appropriate allocations to equities and bonds, will help you outperform inflation in the long term.

More From The College:

Get specialized retirement planning knowledge with our RICP® Program.

Get the details of our WMCP® Program.

Diversity, Equity & Inclusion Insights

2023 Women Working in Wealth<sup>SM</sup> Summit

Over 180 women and their allies from across financial services attended the event in New York City on International Women’s Day. Presentations and discussions covered a variety of topics, ranging from education, changing perspectives, and self-care to rising interest rates and economics.

“You don’t necessarily have to be the subject matter expert. You need to have great leadership skills that are transferable.”

— Kristin Lemkau, CEO of J.P. Morgan Wealth Management

Speaking to a packed room of leaders and practitioners, CEO of J.P. Morgan Wealth Management Kristin Lemkau emphasized that employees and clients are critical to an organization’s success. “I think a person is a sum of their parts,” she said, and “you have to care about the whole person.” She also spoke about team building and stressed the importance of starting with the right people. Lemkau advised aspiring female leaders in the audience that acquiring leadership skills and focusing on organizational growth is critical to career advancement.

Our CEO, @KLemkau closed out the 2nd Annual Women Working in Wealth Summit to discuss her career and driving growth at J.P. Morgan Wealth Management. @TheAmerCol pic.twitter.com/Ms0Ehrz9h5

— J.P. Morgan Wealth Management (@JPMWealth) March 16, 2023

Informed industry experts discussed the future of financial services

Presentations covered a range of topics, with insights including:

- As part of the practitioner breakout: “Catching the Philanthropy Wave with your Clients Estate Planning Essentials,” Dien Yuen, JD/LLM, CAP®, AEP®, executive director, Center for Philanthropy & Social Impact at The American College of Financial Services, reminded the audience to ask the question about philanthropy to everyone, and often, and ask business owners what’s going to happen to their business when they aren’t here. Figure out what the client is trying to do, and then figure out the tools in order to do it. These important questions all need to be addressed. She stated you can gain access via greater education and applied knowledge, and then become a “lifelong learner.”

In the practitioner breakout: “Alternative Investments Post-FTX,” panelists stated that the average individual has no access to an immediate money transfer while explaining that it’s expensive to be poor. There are still secrets around money and investments, along with deep historical roots, and panelists believe access is what drives people to gravitate toward crypto markets.

Tyrone Ross, Jr., CEO/co-founder of Turnqey Labs, urged advisors to “meet clients where they are” to guide their journey forward. He mentioned that portfolios were first derived in the 1940s and they weren’t informed by research, which can further fracture a client’s knowledge base and experience with investing. This requires making financial services accessible to more people in order to change the lens and perspective of wealth management.

Kelly Ann Winget, founder, Alternative Wealth Partners, believes it only takes one person to make a difference, and eventually mindsets shift while you uplift and mentor the next cohort of women on your heels. She challenged those in the audience to be someone to stand up in the room for what they believe. “You are here saying you want to support women, but are you a “way” maker? You have to be willing to change the narrative. When you have the power to anoint a woman to put her in power, you have to do it.” Her message was to “be the little flame within the organization” and make a way while serving as a beacon for others.

In her leadership breakout: “How to Get Ahead of Burnout, Read the Signs, and Assess the Risk,” author and burnout expert Cait Donovan conveyed that companies are now changing their corporate culture in as few as 3 years, immersing employees in cycles of constant change. She highlighted workplace risk factors for burnout as: workload, lack of community, lack of control/autonomy, lack of fairness, lack of recognition, and values mismatches.

Donovan emphasized that the best companies out there are practicing psychological safety, are aware of burnout risk factors, and support team members in need while she acknowledged the importance of advocating for and advancing women in the industry.

Wonderful start to the day hearing from @TheAmerColPrez and Kristi Rodriguez at the @TheAmerCol Women Working in Wealth Summit. pic.twitter.com/YUvbI34e5n

— Mary Kate Gulick (@MaryKateGulick) March 8, 2023

Staying in the struggle and the state of progress

The American College of Financial Services President and CEO George Nichols III, CAP®, addressed the audience by invoking Frederick Douglass’s quote, “If there is no struggle, there is no progress.” He acknowledged the progress already achieved and left the audience with compelling questions: “How do we stay in the struggle and advance the progress? And how do we determine the voids we’re trying to fill?”

Nichols invited everyone to engage with the Center for Women in Financial Services to define the voids and meet those needs. By doing so, advisors can better focus on their clients. He believes “it cannot be about ‘what you sell,’ but rather, it has to be about ‘what they need.’”

Women Working in WealthSM Walk advocates for pay equity

Director and Chair Lindsey Lewis, MBA, ChFC®, CFP®, of the American College Center for Women in Financial Services kicked off the annual event by leading a brisk morning walk to the “Fearless Girl” statue on Wall Street. The walkers struck their best power poses with “Fearless Girl” while a placard reminded everyone why the meeting was so important, reading: We won’t overcome pay inequality for 300 years unless we do something now.

Five Women Working in WealthSM honored for uplifting women

The Center for Women in Financial Services announced a list of accomplished and dedicated women in the profession honored as this year’s Women Working in WealthSM Award recipients. Created to showcase and celebrate women who have rolled up their sleeves to advance women in financial services through mentorship, sponsorship, and advocacy, each award winner documented concrete examples of how they removed obstacles, aligned with allies, and executed novel solutions to improve gender parity. The 2023 group of award recipients includes:

- Natalie Baires, WMCP®, JPMorgan Chase

- Lauren Oschman, CFP®, CDFA®, Vestia Personal Wealth Advisors

- Sahar Pouyanrad, EMBA, CTFA, AEP®, CEP®, ChSNC®, PFP®, JPMorgan Chase Bank

- Raquel Tennant, CFP®, 2050 Wealth Partners

- Andi Madden Wrenn, AFC®, Zeiders

Speaking at the inaugural @TheAmerCol’s Women Working in Wealth Summit and Awards Ceremony last year was a POWERFUL experience. This year, I hope you'll join me, my @2050WPs & colleagues from across the country to celebrate #FinServ women! #WWW2023https://t.co/f4Rc7IcGng pic.twitter.com/ZCMG2oVA5K

— Lazetta Rainey Braxton, MBA, CFP® (she/her/hers) (@lazettabraxton) February 20, 2023

Great to be taking a deep dive into economic challenges during the closing panel at the American College’s WOMEN WORKING IN WEALTH SUMMIT, 4/7-8, NYC with Sitara Sundar and Carly Doshi, managing director, Wealth Planning @jpmorgan. @FAmagazine https://t.co/SDv3hjSB4U

— Tracey Longo (@TraceyFAMag) March 6, 2023

“Today is such a good day to change the world.”

— Hillary Fiorella, Executive Director, Center for Women in Financial Services

As a proud leader, Hillary Fiorella, executive director for the American College Center for Women in Financial Services, exuded excitement for all the women in the room working in financial services, along with their allies who play an essential role in advocating for and advancing women.

She also reminded everyone that the work is still unfinished because it “takes 30% longer for women to get promoted to the C-suite.” She pointed everyone to the Center’s research to help determine if it is more effective to stay in the same firm or to move around to different firms to receive promotions.

CFP Board Director of Diversity & Inclusion Dawn Harris connected w/ CFP Board volunteers at the #WomenWorkinginWealth Summit! From left to right, Diversity Advisory Group Member Rianka Dorsainvil, CFP® (@Rianka_D), Dawn, & Women’s Initiative Council Member Angela Ribuffo, CFP®. pic.twitter.com/YkEFuux9Qo

— CFP Board (@CFPBoard) March 8, 2023

During the Women Working in Wealth Summit held by @TheAmerCol, recruiting experts discussed how as women prefer remote work, firms need to learn how to adapt to create a more inclusive and diverse workplace. #diversity #women @ericacarnevalli https://t.co/uhjllqRsGm

— Financial Planning (@finplan) March 10, 2023

See the recap video from our event:

A New Team Spirit

For The American College of Financial Services, these events were a litmus test for a culture change already underway. While that growth is ongoing, The College has significantly strengthened its bonds with employees.

Since 2015, The College has utilized internal surveys to measure employee engagement and take the temperature of its faculty and staff. The results of the first survey conducted during President and CEO George Nichols III’s tenure in 2019 showed low engagement and uncertainty, so College leadership committed to addressing areas of concern.

College leaders immediately implemented a three-point plan for cultural change. First, they shared the survey results with the entire College to ensure greater accountability and transparency. Next, they began the process of forming a Culture Committee with representation from non-supervisory faculty and professional staff, including an HR representative with facilitation from an external consultant, to recommend improvements in the workplace environment. Lastly, they solidified cultural improvement as an ongoing strategic initiative for The College, making building a better culture one of its highest priorities.

The results were seen quickly – and as Deborah Eskridge Glenn, MA, MSM, SPHR, SHRM-SCP, Vice President of Administration, and Chief Human Resources Officer attested, they spoke for themselves. “In 2020, our engagement score with employees improved by 38%, and since then, we’ve continued to perform above local and national engagement rates,” she said. “Due to our elevation of cultural change as a strategic initiative, employees at The College now use words like ‘inclusive,’ ‘evolving,’ ‘engaging,’ ‘transparent,’ and ‘positive’ to describe our culture.”

When compared to its peer organizations, The College can now be found in the top 5% of surveyed employers in the Philadelphia area in terms of work-life balance and clued-in employees. It also ranks in the top 25% when looking at qualities such as supportive managers, trusted leadership, strong values, open-mindedness, innovation, employee appreciation, and company direction. The most visible effect of The College’s cultural shift, however, has been its identification as a Top Workplace in the region by The Philadelphia Inquirer – not once, but twice – in 2021 and 2022.

While the recognition has shown The College’s focus on culture works, those involved in the change are not resting on their laurels, and many initiatives to continue cultural change are ongoing. In 2022, The College conducted its first Diversity, Equity, and Inclusion (DE&I) survey for faculty and professional staff, the results of which were used to develop a formal Diversity, Equity, Inclusion, and Belonging Committee and program dedicated to allowing employees to bring their whole self to the workplace.

Karen Cerino, a Senior Video Editor in the Marketing and Communications Department and a member of the Culture Committee, says there are three primary areas the group has focused on in terms of improvement. “In the past year, we’ve worked to develop problem statements and identify areas where we can affect positive change,” she said. “The first is meaningfulness: do you feel your work is important? The second is interdepartmental cooperation: are we all working together and collaborating as effectively as possible? The final one is execution: are we doing what we say we’re going to do regarding following the recommendations we make? Having a voice from every department on the committee has really helped improve our communication and process.”

Glenn says organization-wide All-Hands meetings are just one of the methods The College has used to approach the biggest institutional challenge to cultural growth: building trust. “Institutional change requires identifying issues, developing action plans, and executing those plans,” she said. “You can’t just be satisfied with data. You have to focus on fully operationalizing those cultural strategies to be sustainable now and into the future. More frequent and open communication has helped show people we’re being transparent and we’re listening to them.”

While much has been accomplished, it is understood new challenges will always arise for The College to overcome in its constant quest to improve workplace culture. “Historically, The College has been a learning culture,” said Glenn. “Now, we’re moving toward a more results-based culture where we try to balance structure and accountability in an environment that’s friendly and welcoming to faculty and staff. In 2023, we’ll focus on solidifying a culture of assessment, both academic and institutional.”

Read this story and more in our 2022 President’s Report.

RIA Disruption

What began with only a few financial advisors partnering up in the city of Akron, Ohio has become a multi-branch business with 180 team members serving 5,500 households with a full spectrum of services from retirement and business planning to comprehensive family planning. The firm has grown by almost 4,000% in under two decades to manage over $10 billion.1 Sequoia Financial Group has also been part of numerous prestigious industry listings including Barron’s Top RIA Firms, Crain’s Investment Advisers List, WealthManagement.com’s Thrive Awards, the Inc. 5,000 List, and more.

What has powered Sequoia Financial Group’s success in a highly competitive industry? According to its team members, the answer is simple: the specialized knowledge, skills, and education they gained through The American College of Financial Services.

One only has to speak with the advisors at Sequoia Financial Group for a few minutes to realize they have a focus on furthering their education that powers everything they do. To them and many other professionals, it is a must in a marketplace crowded by not only other RIA firms but the industry behemoths and their offshoots they are often forced to compete with.

“Our team members enhance the growth of our firm with higher education, and it empowers us to attract clients with more complex situations and deliver them great advice that keeps them around,” said Bill Venter, CFP®, CIMA®, AIFA®, CEPA®, Senior Client Advisor at Sequoia Financial Group. “Education is a competitive edge. If you’re not growing through education, we believe you’ll lose that edge eventually.” Venter himself completed the education program that prepared him to earn his CFP® mark through The College.

It is not just a matter of prestige, however: team members at Sequoia Financial Group say they have noticed firsthand the respect designations and certifications carry, especially those from The College.

“My biggest a-ha moment came when I was working with a prospect who was deciding between one of our competitors and us,” said Dave Massare, CFP®, CLU®, Vice President of Private Client Services. “When they made their decision, they told me the letters behind my name made a big difference because our competitor didn’t have them. I know a lot of other advisors without designations who are really good and just haven’t bothered to take the courses and sit for the exams – but prospects don’t know that. If I have two designations and our competitor has none, they see them as a level down.”

Sequoia Financial Group is not the only firm that has achieved scale through specialization. Terry Parham, CFP®, ChFC®, RICP®, WMCP®, CLU® and Kennah Parham, CFP®, ChFC® are a husband-and-wife team working together at Innovative Wealth Building, an RIA firm based in California, MD. Both have been through multiple College programs, and they say the experience has changed their personal and professional lives.

“One thing that led us to pursue the RIA model was flexibility: wanting to provide better services, have better technology, stronger investment options, and more control and accountability,” said Terry, Managing Partner at the firm. Because of his desire to specialize in investment strategies, he embarked on The College’s Wealth Management Certified Professional® (WMCP®) Program – which made a world of difference.

“The WMCP® gave me an adrenaline shot of confidence, knowledge, and higher-level thinking,” he said. “Just by slightly tweaking my approach to advice, I saw tremendous changes.”

Kennah, the firm’s Chief Technology Officer, agrees with her husband’s assessment. “To me, it felt like The College was the premiere educational experience in our industry,” she said. “They’re the trendsetters, are top-of-mind for many people, and come highly recommended.”

Kennah completed The College’s CFP® Certification Education Program. “Realizing how much knowledge I didn’t have before earning the certification was so eye-opening and impactful,” she said. “It expanded my mind and opened me up to many different planning paths I didn’t even know existed.”

Sequoia Financial Group and Innovative Wealth Building are far from alone in their experiences. In a flash survey of roughly 500 independent advisors across the country taken in May 2022, over 90% of respondents said designation, certification, and degree programs have helped advance their career – and 75% said the CFP® mark, while important and well-known in the industry, is not enough to guarantee success.

Respondents overwhelmingly desired further education on specialized topics such as retirement income planning, investment and wealth management, estate planning, and advanced tax planning. In fact, specialized knowledge was ranked by respondents as their leading business concern, even greater than having the best technology. This desire for specialization in diverse planning areas demonstrates a need in the RIA space The College is well-equipped to fill.

“Additional education beyond my CFP® certification was very enjoyable,” said Stephen Pomanti, MS, MSFS, CFP®, ChFC®, CLU®, Financial Planner at McLean Asset Management in Tysons, VA. “Being surrounded by people with a shared passion for your craft and different perspectives and experiences is wonderful. I’m employing the education I got from The College and applying that knowledge directly in practice with my clients daily.”

In an industry that often struggles to retain talent, the team at Sequoia Financial Group puts a premium on career advancement opportunities within their firm to attract, cultivate, and keep new professionals. Specialization through further education is a big part of those efforts.

“When I’m talking to someone who wants to be a part of our team, it definitely sets them apart if they have a designation or degree from The College,” said Kristen Kartisek, MBA, CLU®, Director and Senior Recruiter. “We have developed our own career progression, and agreeing to enroll in a College program is a huge part of that.”

Indeed, business growth is foremost on the minds of emerging RIAs as they seek to secure more clients and a larger market share through recruitment and planning. 64% of respondents to The College’s RIA survey said they planned to add up to five new team members over the next three years, and over a third cited organic business growth as their #1 priority. Tellingly, 67% of those professionals also said professional designations are key to powering that growth.

“Designations are like rocket fuel,” said Scott Winslow, MSFS, ChFC®, CLU®, RICP®, AEP®, CCFC, Managing Partner and Investment Advisor Representative at Nabell Winslow Investments & Wealth Management. “Having them behind your name propels your career, without a doubt. You become more confident without even realizing it – but your clients do. They show you have the confidence to address their concerns and that you’re serious as a professional.”

Winslow said ongoing development through education is a key focus for his firm. “Many of the top people in the field are heavily credentialed, and I knew I wanted to follow their example and gain the skills I needed to get clients to the finish line,” he said. “We have three partners at our firm, and we all have three or more designations. The CFP® mark and the Chartered Financial Consultant® (ChFC®) designation are great starting points. Still, you really need the specialized knowledge that will give you a leg up immediately from programs like the Retirement Income Certified Professional® (RICP®), Chartered Life Underwriter® (CLU®), or WMCP®.”

One of the advantages of RIA firms offering specialized services is the family atmosphere many of them promote: a team of advisors working together, each with different expertise, to give clients the best experience possible and resolve any concerns they might have. Many of these advisors say they’re proud to work in an environment where collaboration rather than competition is encouraged. If they do not have the answer to a particular question, they just walk down the hall to find someone who does.

Independent advisors surveyed by The College testified to the importance of service integration as helping them become more efficient, client-centric, and profitable. Advisors say they see integrated services as table stakes, keeping clients in-house to cultivate longer-lasting relationships for the entirety of that client’s life. Nearly 80% of survey respondents said knowledge gained from designation programs supports service integration – a key figure.

“Pursuing specialization through The College gave me the expertise I needed to dig deeper into our clients’ complex planning needs and grow in my career,” said Heather Welsh, CFP®, AEP®, MSFS, Vice President of Wealth Planning at Sequoia Financial Group. “No one can be an expert in every area, so we have team members who hold the RICP®, CLU®, and other specialized designations. It’s a great comfort knowing they’re there, and when a nuanced question comes up, they automatically spring to mind.”

The Sequoia Financial Group family has leveraged The College’s varied program offerings to branch out into diverse areas of specialization. Their success shows the commitment has delivered a sound return on investment.

“The world today demands personalization, and our clients want advice delivered through technology, as well as specialization driven by education,” said Trevor Chuna, CFP®, AEP®, CTFA, MSFS, Chief Technology Officer. “There’s a lot of talk about how technology makes us more efficient and powers business success, but to me, the greatest driver is actually the specialization The College offers which, combined with our technology, creates unmatched client experiences.”

Advisors at other RIAs agree that a one-stop-shop for all a client’s financial planning needs is extremely helpful, and a big part of what has made their business grow and thrive.

“To be able to walk across the hall when you need help on something is a great feeling,” said Venter. “That team environment is a big part of our culture.”

“None of us is as smart as all of us,” Terry adds. “Collective wisdom and expertise elevate your value and the experience of working with you for clients, and that’s how you get them to stay and grow with you.”

With tens of thousands of United States managing trillions of dollars, independent advisors and their practices will no doubt continue to disrupt traditional business models – and we look forward to seeing and supporting how they innovate and thrive.

Access interviews with the advisors featured here in the 2022 President’s Report.

1AUM as of 5/1/2022.

Equipping an Industry for Disability Planning

What about the continued mental challenges that go with those ongoing physical challenges — for the person, for their loved ones? Or, what about the barriers you can not see? And of course, what about the costs? The price of mental or physical challenges can be daunting and often include providing personalized therapy or care beyond adapting someone’s physical surroundings.

What happens when someone without disability benefits suddenly needs this level of personal and extra care? Most adults are not prepared for sudden and unexpected disability. Out-of-pocket costs can be quite prohibitive, not to mention how draining they can be on the family’s assets and reserves. Whereas, if someone does receive disability income, those benefits can be jeopardized by choices a loved one might make because they think they are helping.

If you or someone you love happens to be impacted by a disability, you need guidance and advice, action plans, and next steps. You also need to understand regulations and how money moves made by you or someone close to you could impact your eligibility or standing for services that you need or expect to need in the future.

If you are a financial professional, you better get it right when your clients need this level of expertise because the need is great and growing along with an aging population. According to the CDC, as many as 61 million adults are living with a disability, and to meet the long-term care needs of Baby Boomers, financial professionals need to up the ante on their education and eliminate knowledge gaps in short order.

This is what Joellen Meckley, JD, MHS, executive director of the American College Center for Special Needs, considers daily. From firsthand experience, she understands that there are misconceptions about resources available to those with disabilities and that disability is not a small, niche practice area for financial professionals but necessary knowledge needed by all those who provide financial guidance.

“The financial services industry has done a disservice in its failure to adequately train and prepare professionals to recognize and help address the issues faced by those living with disability,” states Meckley.

While explaining that people with disabilities represent the largest minority population in the United States, Meckley admits she has steep ambitions and hopes to change the perception of and value placed on special needs disability and long-term care planning throughout the industry. She sees three major steps forward.

#1. Education Throughout a Client’s Lifespan

The first promotes expanded research, thought leadership, and education for planning for disability throughout the entire lifespan, as well as a disability that unexpectedly occurs in midlife or later. In her own practice, Meckley tried to involve a client’s longtime financial advisor in the planning process. She found that advisors often lacked a realistic understanding of the actual cost of caregiving or long-term care service.

“Many of them didn't know about the various options available to their clients,” Meckley said, “and thus they couldn't really help sort through those options from a financial perspective.” She explained a shift in the Center for Special Needs’ focus to expand its educational offerings scope to serve the entire population. Meckley believes planning for families with special needs children will always “remain a key area of expertise for us, but the reality is that adult-onset disability is also more common than people realize.”

Adult individuals and their caregivers are also desperately in need of financial advice to help them deal with what is often drastically changing circumstances in their lives, according to Meckley.

#2. Access to Just-In-Time Learning

These needs also open opportunities within the profession for her second step, ensuring high-quality educational options are easily accessible by developing more continuing education programs and modularized learning opportunities for anyone who wants to better serve this population.

Meckley elaborates how advisors in the field repeatedly tell her there is simply not enough support for them in terms of training. Since only limited and hard-to-find topical issues are available through legal services programs, Meckley sees this as The College’s opportunity to fill that gap, even if that is through continuing education and partnership opportunities with advocacy groups that are doing incredible work.

The primary goal for her initiatives is to “spread awareness about the planning and business opportunities that are available to those who are looking to serve these clients.” She believes that all advisors need a better base understanding of these issues and that it takes someone who is comfortable with going beyond finances to discuss difficult subjects.

Financial professionals, according to Meckley, “are craving better and more in-depth complex advice so that they can pass it on to their clients.”

#3. Consumer Education that Drives Deeper Community Connection

Her third goal is intended to alter how financial professionals serve those impacted by disability. Meckley plans to develop educational resources that are delivered directly to consumers, or those who are directly impacted by disability, so that more clients and their advocates can be better informed. She states, “the Center can play a strong role in promoting greater financial knowledge and financial security within the community itself.”

The best client is a well-informed client, says Meckley.

“Informed clients understand the value in hiring an advisor who truly understands their unique life circumstances,” she states. Through the development of more direct-to-consumer educational options, Meckley hopes to create that well-informed client base. “In increasing awareness of the disability planning opportunities among professionals, more clients are able to find knowledgeable advisors who have the right expertise.”

Educating advisors on how to assist in planning and how to connect families with the other key professionals that they need on their team is also essential. Financial advisors see the scope of how disability and chronic health conditions impact their existing clients. However, once younger clients age out of the support guaranteed to them from the states, many parents struggle to navigate the system for their loved one who is now in adulthood. According to Meckley, “parents need to understand how they can help create a support structure for their child that will last even when they themselves are gone someday… this is really life planning.

“Professionals need to support that wide middle swath of the rest of the industry or country that kind of falls in the middle and are getting neglected.” Clients do not have unlimited resources, but they also do not always qualify for the same benefits. Meckley wants to “help advisors identify where their efforts can be best directed and the areas in which they need more expertise” by working together with The College's other Centers of Excellence. “Research has already shown that disability disproportionately affects women, minorities, and other groups that our other Centers are focused on as well.

“No one can deny the complexity that's required if you are planning for someone who's living with a disability, no matter what phase of life they're in,” Meckley says in discussion about a myriad of issues. “There needs to be a balance between making sure, for example, that someone is provided with the extra financial support that they might need in life while still maintaining eligibility for public benefits. It is in advising caregivers and family members on their estate planning to make sure that with the best of intentions they don’t inadvertently provide financial support to someone that then disrupts their ability to utilize public benefits. There's a need for caregiver advice. There's a need for good accounting advice. Sometimes a family needs a special education advocate because their child is struggling in school and all of these things are tied together. So, it always needs to be a holistic approach.”

“My vision for the industry is that someday quality education related to disability and long-term care planning will be viewed as a fundamental part of any well-rounded financial professional's career,” Meckley says.

Meckley is currently in the process of updating the Chartered Special Needs Consultant® (ChSNC®) Program curriculum to include a wider range of planning issues to incorporate more applied exercises, such as case studies that are designed to teach advisors very practical skills that they can apply to realistic situations. She states there are actually very few quality CE options available for those practitioners who want to gain expertise in disability planning.

“I've heard a lot of stories where there was a lack of planning and unfortunate results occurred. Again, it's always with the best of intentions.” Meckley states, “People are trying to do the right thing, think they're doing the right thing, and it can cause chaos in a situation. You need to plan well and you need to plan early to ensure the best outcome.”

“I think financial services are traditionally viewed by many people as only being designed for a certain type of client or demographic,” says Meckley. “Under The College's leadership, we're seeking to demonstrate that there is an opportunity for the financial services industry to truly be a force for positive change.”

Access interviews featured here and more in our 2022 President’s Report.

Retirement Planning Disruption

In the past several years, major changes in how consumers and financial advisors alike view the world have shaken long-held ideas about planning for a life in retirement. The Covid-19 pandemic, ongoing inflation, and the massive shifts they both ushered in for markets and how we live our daily lives changed our perception of how we interact with others and plan for our future. New legislation from the halls of Congress, such as the SECURE Act, has required professionals and clients to rethink what steps must be taken to avoid running out of money when needed most. And the constant march of progress with advances in financial services technology has presented longtime professionals with new challenges to their client relationships in an increasingly do-it-yourself culture.

As an educational institution on the front line of these landmark industry shifts, The American College of Financial Services and its thought leaders are recognizing the changes and rising to meet them.

“This anxiety about retirement planning has been a long time coming,” said Michael Finke, PhD, CFP®, Director of The College’s Wealth Management Certified Professional® (WMCP®) Program. “As employers have transitioned from pensions to defined contribution plans, individuals bear greater responsibility for turning savings into a lifestyle. We have a new generation of workers, many of whom have saved and invested automatically through target-date funds, who are seeking clarity about how these savings translate into income.”

As the responsibility for funding retirement has fallen more and more to individuals, this has increased the demand for professional advice.

“We now essentially dump a huge pile of money in our clients’ laps and say ‘good luck.’ We expect them to figure out what to do with that money and how to invest and spend it wisely on their own,” Finke said. “Our research shows that ‘understanding how much I can safely spend in retirement’ is by far the number one reason consumers would seek the services of a financial advisor – more than twice the percentage that sought advice to improve investment performance.”

Advisors in the field seem to be picking up on clients’ anxieties. In a survey of representatives from various RIA firms across the country conducted by The College, 71% of respondents said they wanted more retirement planning knowledge to meet the rising demand for these services. The data supports the need for a far more robust focus on retirement from firms and advisors, and one The College’s thought leaders are working to understand through a behavioral and financial lens.

Wade Pfau, PhD, CFA, RICP®, Professor of Practice in The College’s Retirement Income Certified Professional® (RICP®) Program and a field leader in retirement planning and theory, said the practical concerns of inflation, pandemic, legislation, and technology are just the tip of the iceberg – the real issues advisors need to address are psychological ones.

“Covid-19 was a reminder to all of us that life is fragile, and we need to make the most of today: that’s a message that really resonates with those closer to retirement, as well as making younger people think about their futures,” he said. “Our renewed focus on personal health has called into question this widely-held assumption of institutional living in old age: assisted living and nursing homes are no longer the safe places they used to be. Do aging individuals now want to try to stay in their homes as long as possible, which requires more strategic spending and saving? It’s an interesting conundrum.”

Pfau said the most prominent trend he has noticed is that those at or near retirement age are becoming more cautious than they used to be. Uncertainties like fluctuating interest rates, rising prices of goods due to inflation, and drops in bond and stock values have created a “triple whammy” of concerns that motivate people to lock their hard-earned and saved money down – sometimes at the expense of living better in retirement.

“Most financial planning software will tell you to assume a long-term inflation rate of two to three percent, but short-term inflation is much higher than that,” he said. “It’s not a fair comparison, but it makes people nervous about their money and can lead to inopportune decisions.”

Many experts agree that this seems to be the primary modern threat to retirement planning: not running out of money, but the missed opportunities that worry can cause. “Decumulation is much harder than accumulation,” Finke said. “Workers who are diligently saving in their IRA or 401(k) feel they’re working toward meeting a savings goal. But once most get there, they’re uncomfortable seeing the number get smaller to meet the spending goal that motivated the savings in the first place. Of course, you can’t take that money with you, but the fear of running out is so great that people aren’t living as well as they could. They essentially leave joy on the table because they fear losing their nest egg.”

Finke said his research has found most retirees are more comfortable spending guaranteed income such as pension plan money and Social Security, but less so money they have saved up themselves. Political instability, inflation, and general market insecurity top the list of anxieties for most of today’s high-net-worth earners – all concerns connect to how far people’s savings and preparation will go in retirement today. This, however, is where expertise in retirement planning can step in to fill the breach, especially from a personal perspective.

“The best gift an advisor can give a client trying to plan their retirement is the confidence to spend the money they saved – it’s why they saved it in the first place,” Finke said. “Clients need good advice, but even more, they need a comforting voice they trust telling them it will be okay. By specializing in retirement planning, advisors will have an advantage in building those kinds of relationships moving forward and fostering more trust with their clients through that greater level of clarity.”

Under Pfau and Finke’s leadership, The College’s RICP® and WMCP® Programs have developed complementary approaches to the disruptions of modern retirement planning. In WMCP®, students learn the various methods helpful to asset accumulation in preparation for retirement, including ideal investment vehicles and ways to build portfolios that stand the test of time. Then, in RICP®, they learn how to take those assets and efficiently draw them down over time, and gain unique knowledge on long-term care issues, tax considerations, and more. But The College is not just using facts and figures to influence its approach to change how professionals and clients view their retirement planning: it’s also a question of philosophy.

“Historically, account-based strategies have been the most popular in retirement planning: allocate money into stocks and bonds, and then gradually withdraw a certain amount every year at an agreed upon percentage like the ‘4% Rule,’” Finke said. “These days, it’s not all that clear those old rules are still effective, so we like to promote a goal-based planning strategy: start with learning more about your client’s goals and then develop a strategy that works for them and meets those goals. Planning shouldn’t be blind to the reality of how clients want to live, and working through this process with their advisor gives them a better understanding of whether the market will impact a client’s desired lifestyle.”

In the RICP® Program, Pfau has supplemented new and familiar concepts in retirement planning with his research on the idea of retirement income styles. “There’s a growing recognition that any strategy can be viable, but only for the right client,” he said. “Are they comfortable spending from a broadly-diversified investment portfolio? Would they rather use a ‘bucketing’ technique to invest differently for short-term versus long-term growth? Or do they want to build a protective floor first and then build on top of that to protect their essential needs against discretionary spending? It all depends on the client, and advisors must customize their advice for each client. We can’t afford to be stuck in a one-size-fits-all mentality anymore.”

Thought leaders like Pfau and Finke are also constantly updating The College’s programming to coincide with the latest regulatory and logistical changes – and 2022 has been an eventful year. From the myriad changes of the SECURE Act and its recent 2.0 incarnation to elemental retirement planning to the elimination of the stretch IRA and new limitations of withdrawal time horizons for required minimum distributions (RMDs), faculty have been kept busy speaking with industry leaders and conducting research on what the shifts in the planning landscape mean for students, advisors, and the general public. They are already planning to make curriculum changes in response to the passage of the updated SECURE Act 2.0 in 2023.

One change Pfau sees is the need for a more consistent focus on tax planning in retirement income education. “Sequence of returns risk has become a front and center concern. It’s not an abstract concept anymore,” he said. “When the SECURE Act changed the game for IRAs and limited the lifetime stretch withdrawal to a 10-year period, a lot more people became potential candidates for tax jeopardy and losing much of their hard-earned savings without proper planning steps to limit tax deductibility. Now, we’re seeing people in their peak earning years who may be in higher tax brackets needing to consider Roth conversions and other measures much earlier than before if they want to pay taxes at the lowest possible level.”

Pfau said clients with trust holdings with RMDs should revisit their estate planning documents frequently to ensure the trusts are still working as intended. He also noted buffer assets – not part of an investment portfolio such as a bank savings account, cash value whole life insurance policy, or a reverse mortgage that can provide temporary but fully liquid income at times of market upheaval – are growing in importance to consumers. Advisors, he said, should also be talking about these assets if they want to fully future-proof their clients’ retirement planning.

For Finke, one of the biggest disruptions the past few years have brought to traditional retirement planning has been the advent of technology as part of the process – but it’s not all robo-advisors and retirement planning automation. “In our surveys, we’ve asked people how comfortable they are seeing financial advisors via Zoom or other remote conferencing methods,” he said. “It’s become quite popular since the onset of the Covid pandemic, and many advisors have adjusted to this new reality of communication. We find while most clients want to meet with a new advisor in person for the first time, most people are okay with virtual meetings after that and, in fact, prefer it. When you’re using Zoom to meet with your advisor, you don’t have to take the time and inconvenience to travel to see them at their offices, and in some ways, it makes those relationships even easier to maintain.”

However, Finke cautions that advisors cannot become complacent in today’s world with the myriad options that are available to clients to do their retirement planning themselves. “While it may not always be advisable, it’s relatively easy for consumers to go it alone if they want to,” he said. “We as advisors need to show them that we can communicate with them on a different level to prove our value – to find out what they want to achieve, quell their fears, and help them succeed. Technology is here to support advisors, not compete with them. Still, even people who understand they shouldn’t worry about their portfolio returns constantly sometimes need the voice of another human to tell them not to. That’s something technology can’t do for us.”

In looking ahead to the next potential retirement planning disruption, many industry leaders have pointed to legislation or regulatory surprises, from tax reform to needed changes to the Social Security program. Things are never certain in retirement planning, Pfau said, and it is wise to keep an eye open for things that could cause the next shakeup. However, he said he is more optimistic about the future of retirement these days, especially as advisors look to focus more on people-centric relationships rather than purely transactional interactions.

“The situation is getting better. The Inflation Reduction Act has done a lot to lower prescription drug costs and take the financial burden off retirees in other ways,” he said. “The behavioral finance knowledge we preach here at The College also shows tomorrow’s advisors that clients may want different kinds of relationships with them. Some people want to delegate and have a knowledgeable advisor decide for them. Others want their advisor to be a partner in their planning and be more involved and educated about what’s going on. Still, others are what I might call ‘validators’: they’re not ready for a full-service relationship with an advisor, but they want help with a specific planning or money management situation that’s important to them. Advisors need to have different models and approaches based on the different kinds of relationships clients may be looking for.”

In addition to the Inflation Reduction Act, Congress passed the highly-anticipated SECURE 2.0 Act in December, which Pfau and Finke pointed to as another critical piece of industry-shaping legislation. The act continues the government’s reshaping of retirement planning that started with the SECURE Act of 2019 and stands to further the disruption of retirement as many know it.

Among other key provisions, the two SECURE acts increased the age at which consumers are required to take RMDs from their retirement accounts, in part an acknowledgment of the longer lifespan of the average American and also to account for worries about taxation on saved dollars. With RMDs pushed back, many clients will have more time to work with their financial advisor on optimal retirement strategies and may be in a lower tax bracket, meaning they can keep more of their hard-earned savings; however, this also means a renewed focus on tax planning within the retirement planning space advisors would be well-served to prepare for.

Many headlines have focused on the act’s mandatory and automatic enrollment for most employees in their company’s 401(k) or similar retirement plans. By making enrollment in these plans automatic, Finke said his concerns about the government or businesses putting the onus of retirement planning on individuals could be at least partially alleviated, and more employees – especially those working in lower-wage jobs – could be empowered to begin building up assets for their future financial security. It also means a greater opportunity for financial professionals focusing on retirement planning to access a growing demand pool for their services.

Along with these changes, the act also loosens penalties on emergency withdrawals from retirement plans, which have typically come with a heavy tax burden. While it is rarely optimal to take money out of a retirement account early, sometimes the situation requires it. The additional leeway will likely give consumers greater peace of mind in their conversations with financial professionals.

With much of the Washington focus of late on the details of student loan debt, another portion of the legislation allows for employer matching of student loan repayments. With the price of higher education increasing, many young Americans are saddled with crushing debt that hangs over their heads for decades. Experts say offering incentives to employees regarding paying off student debt could also open the door for those same employees to invest more heavily in their retirement plans – another source of increased security and demand for financial advice. All these and more changes will be incorporated into the College’s curriculum, including WMCP®, RICP®, and the Ed Slott and Company’s IRA Success program.

As an authority in the financial services field for nearly 100 years, The College has always prided itself on changing with the times, adapting to new situations and realities like these in the industry, and updating the education it offers to keep up with the latest facts on the ground. It is what faculty members like Finke say sets The College and its programs apart.

“We don’t just teach content: we teach application,” he said. “Having the knowledge of how to build a portfolio or how to plan retirement is just the first step, and this is something up-and-coming advisors are recognizing more and more. Knowing how to talk to clients about these issues and challenges is the key to forming relationships that last into and through your clients’ retirement years.”

Read this story and more in our 2022 President’s Report.

Michael Finke’s Insights

Wade Pfau’s Insights

Five Questions with Chet Bennetts

A veteran of the financial services and education fields as well as the United States Marine Corps, Bennetts holds a master’s degree in family financial planning and is working toward a PhD in personal financial planning while serving as an assistant professor of financial planning at The College and a guest faculty member at the University of Nebraska – Lincoln.

We asked Bennetts five questions about his career, his path to the financial services profession, and what he hopes to accomplish as a faculty member at The College.

How did you come to be involved with The College?

After serving in the U.S. Marine Corps, I was a Colorado native living in a small town in Nebraska where no one shared or knew my name. I needed to stand out among other financial services professionals, and designations seemed the answer. No one around us had their CFP® mark, so I took The College’s program to prepare for the exam. During that time, I realized how well The College’s other programs, like the Chartered Financial Consultant® (ChFC®) and the Chartered Life Underwriter® (CLU®), dovetailed with what I was doing, so it seemed like a waste not to earn those too. Soon I was leading a merger of practices and becoming a top-performing advisor and manager in the company, and I made it a point to create study groups for my new advisors to earn their CFP® marks and ChFC®s as well.

Working for The College is a dream come true for me. I always wanted to join academia, and I looked up to College experts like Michael Finke, Wade Pfau, and Ed Slott. I’m blown away by this opportunity to collaborate with them, especially regarding behavioral finance and how helping someone achieve financial well-being assists them throughout their lives.

As a veteran-turned-advisor, what do you think makes military members and veterans well-suited for this field?

A few key tenants of military service are knowing yourself and your weaknesses and seeking improvement to succeed. When you apply that to the financial services realm, the solution is largely what we do here at The College. We give people a chance to stand out among their peers and for their clients, and we offer an appealing challenge that speaks to the team-building strengths of service members and veterans.

In my view, the perseverance and ability to overcome adversity most military members share is what gives them an advantage in a field like financial services, and I think more service members and veterans would do well to join our industry. You can still help people and make a difference in your community and people’s lives while enjoying the benefits of higher pay, a more flexible and comfortable lifestyle, and less physical danger of course.

Since beginning your work toward a PhD in personal financial planning, what have you learned that other advisors should know?

When we ask people what their sources of stress are, the biggest ones are usually money and relationships – and if you dig deep, relationship problems are often caused by money. Humans don’t handle stress very well. We have coping mechanisms, many of which are unhealthy and only make the problems worse.

As a financial services professional and veteran, I see that daily in our society. While the VA offers various physical health services to address issues like PTSD, financial stress was never a core part of the conversation. I found the academic community wasn’t talking about it, so I decided to focus on the issue of financial empowerment specifically.

How do The College’s CFP® Certification Education Program and ChFC® Program work together to enhance advisors’ skills?

When you take the CFP® exam, you’re telling people that you want to be part of an organization and a body of financial services professionals who hold themselves to a higher standard of excellence. You’re using the exam to prove a set of technical expertise you hold to serve clients ethically. The difference between that and other certifications is how you apply that knowledge.

A ChFC® still has the same base level of knowledge but may apply it differently based on the niche they want to serve. That’s shown by our ChFC® Program having all the same requirements as our CFP® Certification Education Program but with one additional course specifically focused on specialized knowledge and application. We take the core concepts that the CFP® mark entails and show people how they can apply that knowledge in ways that matter to them.

Do you have any pieces of advice for today’s up-and-coming financial professionals?

You’ll never know everything; the moment you think you do, everything will change. Formal education and designation programs are extremely important because they give you a broad knowledge base, but continuing education and keeping your expertise up-to-date are how you stay on track.

The benefit of learning from The College is that we have all this accumulated knowledge and expertise right here. Using that will make you much more successful than trying to do it alone. Don’t get ready to get ready: go do it and dive into the field while at the same time working on a designation or certification. You will build confidence in yourself while becoming more successful in your practice, creating more confidence to power the rest of your career.

An Advocate for Financial Education for Veterans

“We were among the first teams inserted into urban areas, and we were involved in door-to-door combat,” he said. “We were told to expect at least 30% casualties and nearly everyone would probably be injured. In the end, those estimates were pretty accurate.”

Bennetts was among those wounded during the campaign, and after being medically discharged from the military, he occupied himself with other pursuits: entering the financial services profession and starting a new career, as well as a new family. However, years later he got a piece of news that once again spurred him to act on behalf of his fellow service members and veterans.

“As of November 2018, I had lost more of my Marine brothers to suicide post-service than in actual military combat,” he said. “That was a real wake-up call for me, and I couldn’t understand why nobody seemed to be discussing this problem from the lens of how personal finances might play a role.”

Now The College’s CFP® Certification Education Program and Chartered Financial Consultant® (ChFC®) Program Director, Bennetts says it’s been long established that service members on the battlefield won’t be as effective if they’re preoccupied with a toothache or something else physically wrong with them – but financial well-being is just as important as physical well-being to maintaining combat readiness.

“It’s just as problematic, and maybe even more so, for a service member to worry about how they’re going to pay their car insurance or afford their mortgage payment,” he said. “The biggest sources of stress for people are usually money and relationships, and if you dig deeper into many of those relationships, the cause is often still money. I found the academic community wasn’t discussing this in the context of preventing veteran suicide, so I decided to go back to school to confront this issue more seriously.”

While Bennetts said programs by the VA to address physical and mental health problems for service members and veterans, including PTSD, are incredibly important to maintain the well-being of those individuals, financial health is often left out of the conversation. In addition, statistics show that over 20 veterans die by suicide daily in the U.S. on average, demonstrating a significant need for more services to support them. Bennetts says “financial empowerment” is an important part of that equation.

While studying for his PhD in Personal Financial Planning through Kansas State University and still focusing on the issue of financial well-being for military members, Bennetts says he was presented with the opportunity to be part of a select group of student veterans who would be able to propose legislation based on their research. He applied for and was awarded one of the Veterans of Foreign Wars’ (VFW) Student Veterans of America (SVA) Legislative Fellowships, earning the privilege of traveling to the nation’s capital in Washington, D.C., and presenting his findings to those in positions to take action on them.

“All the fellows had different ideas to present,” he said. “One student was working on issues surrounding veterans’ housing insecurity. Another dealt with National Guard members’ life transitions if they were called in to deal with a natural disaster. Mine had to do with financial services, financial counseling, and its integration into PTSD treatment. This was the VFW’s national legislative advocacy week, so there must have been at least 500 of us as VFW members participating from every state and territory going to their individual representatives and pitching their proposals to elected officials.”

It appears Bennetts’ proposal caught the eye of the VFW’s Legislative Affairs team, who brought it to the rest of the organization’s leadership.

“I think they realized I wasn’t a 20-something reading off a script and that I was passionate about this issue and knowledgeable on it,” he said. “Before I knew it, it went from me only meeting with people from Kansas and Nebraska to getting a list of every event happening that week and being encouraged to attend as many of those as I could.”

Over the course of several days, Bennetts estimated he met with over 15 elected officials from nine different states, including Senator Bernie Sanders (D-VT) and Senator Jerry Moran (R-KS), a current member of the Senate Committee on Armed Services. And then, things went another step further.

“They asked us to come to the White House for a meeting,” he said. “I was astounded. We had to complete security clearance requests and meet with the president’s Special Advisor on Veterans Affairs. I got to talk with her and her team about how certain record-keeping practices at the VA were stopping us from getting a clear picture of the actual well-being of our veterans. I even became part of the testimony to the Joint House and Senate Oversight Committee for Veterans Services Organizations (VSO). I’m still processing all of it, to be honest. It was a whirlwind but also an amazing experience.”

Bennetts says he plans to continue his advocacy on financial empowerment for military members and veterans and that he’s been inspired by the entire Washington experience.

“When I reflect on the last four to five years of my life, there’s been a lot of uncertainty, especially regarding my journey toward my PhD,” he said. “That week without a doubt relit my fire to keep going, and it was an honor to be part of the conversation.”

Leaving a Legacy

Peter Browne, Howard Cowan, and Maury Stewart pictured left to right.

The American College of Financial Services has been blessed with dedicated alumni and donors that have devoted their professional and personal resources to ensure the future success of The College. These College champions understand the impact of a College education and how it prepares our students to do great things in an industry and world that needs them.

Peter C. Browne, LUTCF®

A life of service and professionalism that exemplified Dr. Solomon Huebner’s client-first philosophy.

Peter C. Browne, LUTCF®, was a longtime leadership volunteer, loyal donor, and consummate champion for The College. He served on The College’s Board of Trustees and was a past chairman of The College’s Foundation Board. He was serving on the President’s Roundtable and actively working to deepen the partnership between The College and Ameritas that he tirelessly cultivated during his career with Union Central, which then merged into Ameritas Life.

Peter’s passion for The College and Union Central was best exemplified through his leadership to help establish the Union Central Larry R. Pike Chair in Insurance and Investments at The College in 2002. Through the evolution of our partnership with Ameritas, The College was able to create the Women in Financial Services scholarship with Women in Insurance and Financial Services (WIFS) in 2021.

Peter received The College’s President’s Award in 2010 and was awarded the Solomon S. Huebner Gold Medal in 2013, The College’s highest honor, and was a member of The College’s Loyalty Society and Legacy Society.

Peter was a past NAIFA National treasurer, president of NAIFA-NY, and president of GAMA. Serving for over 60 years in the life insurance industry, he was honored with countless industry awards and recognition, including the 2015 John Newton Russell Memorial Award — the highest honor bestowed upon a living member of the insurance and financial planning industry. He spent his time and resources to ensure that life insurance professionals had access to the knowledge to grow and has left a lasting mark on the profession.

Howard Cowan, CLU®, ChFC®

Industry leader and mentor that always made time to share his ideas and insights on how to strengthen and grow The College.

Howard Cowan, CLU®, ChFC®, was the Founder and President of Cowan Financial Group, which he formed in 1985 and ran until he retired from the organization in 2009. Over Howard’s illustrious career, he mentored countless general agents and career agents and was recognized with many prestigious industry honors, including the Massachusetts Mutual Life Insurance Company’s highest honor, the National Chairman’s Trophy, for an unprecedented 20 years.

Howard always made time to share his ideas and insights on how to strengthen The College. Howard served on The College Foundation Board for eight years and was a member of the Insurance Review Committee. At the time of his passing, he was a member of The College’s President’s Roundtable, a President’s Circle member, Loyalty Society member, Legacy Society member, and major capital campaign donor to The College. His other awards and accolades included the Masters Club, Leaders Club, GAMA Master Agency Award, GAMA First In Class, Master Agency Growth Award, and

GAMA Hero Leadership Award.

Maurice L. “Maury” Stewart, CLU®, ChFC®, CLF®

A longtime leadership volunteer, donor, and champion for The College and an advocate for life insurance and the financial services industry.

In 1950, after serving our country as a pilot in the United States Air Force, Maurice L. “Maury” Stewart, CLU®, ChFC®, CLF®, started his career with Penn Mutual as a general agent selling life insurance in Topeka, KS.

Because of the transformational impact of his contributions, Maury was a member

of The College’s 2012 Hall of Fame and the 2017 Solomon S. Huebner Gold Medal Winner.

In addition to being a lifelong learner and a former faculty member at The College

and attaining many designations, Maury encouraged the establishment of the

Charles E. Drimal Professorship in Estate Planning. In 2008, he was honored with

the establishment of the Maurice L. Stewart Lecture at The College in partnership with

Penn Mutual. The annual lecture addresses issues critical to the practice of leadership

development and has featured a series of renowned speakers.

Maury’s values and passion for leadership are also reflected in The College’s Chartered

Leadership Fellow® (CLF®) designation. While holding the then named George Joseph Chair in Management Education, Maury substantially strengthened the development of the CLF® Program. As a guest lecturer for many years, he shared his enthusiasm and wisdom with generations of CLF® students, building their competence as managers and leaders.

The Legacy Society

The Legacy Society honors those individuals who have informed The College of their estate gift intention or funded a life-income gift or life insurance policy that will support the future of The College. We are grateful for these individuals who are living out their philanthropic goals through their legacy.

To learn more about how you can support the future of The College through an estate gift, please reach out to Carol Parlin Prushan at carol.prushan@theamericancollege.edu or 610-526-1389.